Cobalt, a metal prized for its qualities in the field of electromobility, is gradually being phased out of batteries. We examine the reasons for this and propose possible solutions for the DRC.

__

MRK Mining

A monthly mining news bulletin produced by Margaret Rashidi Kabamba

For miners and mining and electric vehicles batteries enthusiasts.

TFM – Cobalt Hydroxide

Kobald – Evil Spirit

In the 1500s, Saxon miners searching for precious metals discovered a foul-smelling ore that was rich in arsenic and difficult to process. Believing it to be cursed, they named it “kobald’, which means “evil spirit”. The word evolved and was first used in Latin as “cobaltum” in 1522, then in French as “cobalt” in 1549 by Pierre Belon.

It was not until 1735 that Swedish chemist Georg Brandt isolated cobalt as a distinct element, proving that it was responsible for the blue color of glass and ceramics, and later, in the production of porcelain.

During the 19th century, the industrial value of cobalt increased, as its alloys improved the hardness and heat resistance of steel. In 1938, John Livingood and Glenn Seaborg discovered the radioactive isotope cobalt-60, opening a new chapter in its scientific and technological applications.

What is Cobalt ?

Cobalt is a hard, shiny, silvery-gray metal currently used primarily as a cathode material in lithium-ion and other types of batteries. It is also used in powerful magnets, cutting tools, and high-strength alloys in the aerospace, energy, and defense industries. Cobalt compounds have been used since ancient times as a pigment (cobalt blue) for pottery, glass, paints, and even as a component of vitamin B12.

The number 27 is its atomic number. Approximately 98% of cobalt is extracted as a by-product of copper in the Democratic Republic of Congo, which holds about 80% of the world’s reserves, and in Zambia, etc., from nickel sulfide in Russia, Canada, Australia, etc., or from lateritic nickel ore in Cuba, Indonesia, Australia, the Philippines, Madagascar, etc. As for cobalt produced as a primary substance, it comes exclusively from the Bou-Azzer mine in Morocco and accounts for 1-2% of global production.

While global cobalt reserves are estimated at 7.1 million tons according to the United States Geological Survey (USGS), terrestrial resources are estimated at 25 million tons and those located on the ocean floor at 120 million tons.

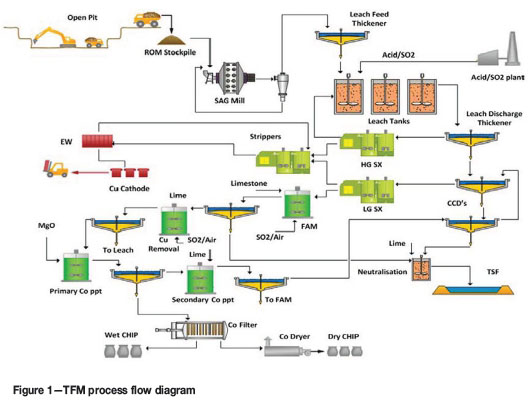

How is Cobalt Extracted from Copper? The Case of Tenke Fungurume Mining (TFM)

The TFM deposit is an oxidized ore containing approximately 0.2-0.3% cobalt, which is mined in an open pit. After crushing and grinding, the ore undergoes leaching, where the crushed ore is mixed with a sulfuric acid solution. This produces an impregnated solution containing copper sulfate and cobalt sulfate. This solution is sent for solvent extraction (SX). An organic solvent is added to selectively capture the copper. This is sent for electrolysis to obtain 99.99% cathode copper. The remaining aqueous solution (the raffinate) is treated to recover the cobalt by neutralizing the pH with lime or soda. This precipitates the residual impurities (iron, aluminum, manganese, etc.). The pH is then raised further, causing the cobalt to precipitate as cobalt hydroxide, which is finally washed, dried, and packaged for export to China, where it is refined to obtain metallic cobalt.

Usage of Cobalt

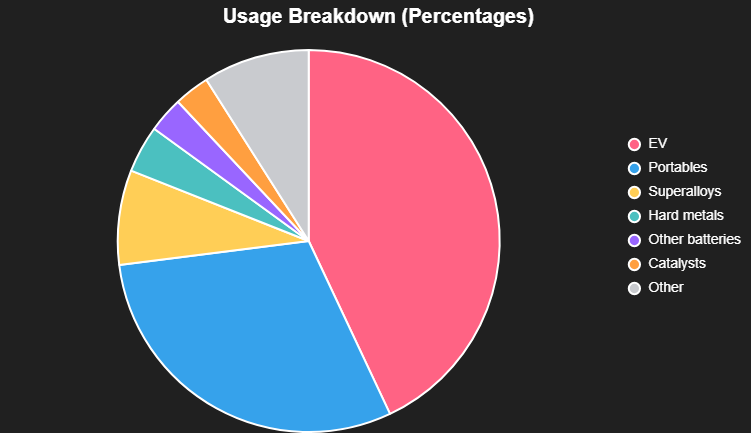

According to the 2024 Cobalt Institute data, here is the percentage of cobalt usage in the world:

43 % in the cathodes of electric vehicles

30% in mobile phones

8 % in superalloys

4% in hard metals

3% as a catalyst in the chemical and petroleum industry

3% in other batteries

9% for other things (pigmentation, soaps, tires, pharmaceutical industry etc.

Who Produces Cobalt in the DRC?

Cobalt is produced in the provinces of Haut-Katanga and Lualaba, and around 80% of this production is exported to China. The production process is primarily focused on low value-added products, including salts, concentrates, hydroxides, and carbonates of cobalt, as well as white alloys. Most of this production is carried out by large international mining operators that have signed partnerships with Gécamines. Please find below the names of the ten main operators:

Kisanfu Mining (KFM),a 100% Chinese shareholding (71% – CMOC; 23%: CATL) contains a very high-grade cobalt deposit. Sold to the Chinese by the Americans for 550 million USD, today, with its metallurgical plant, its revenue exceeds 2 billion USD.

Tenke Fungurume Mining (80% shareholding – TFM Holding & 20% – Gécamines) – combined production by the two companies controlled by CMOC amounts to approximately 36,000 tons of cobalt in 2025. According to the company, from 2006 to 2024, TFM’s total copper and cobalt contributions to the Congolese government reached about $7.026 billion.

Sicomines (Sino-Congolaise des Mines) of the Zhejiang Huayou Cobalt group, one of the largest producers of refined cobalt in China, majority shareholder in Congo Dongfang International Mining (CDM) and Minière de Kasombo (Mikas). CMOC holds a 5% stake in Sicomines, which in 2024 had paid the DRC USD 324 million in royalties and other charges.

Kamoto Copper Company (KCC) and Mutanda Mining SARL (MUMI), (shareholding – 75% Glencore and 25% Gécamines). In 2024, Glencore had paid a total of USD 524.628 million to the Congolese government (2024 Payments to Governments Report). Glencore is the only mining operator in the DRC that produces refined cobalt.

The Kazhak Eurasian Resources Group (ERG), operator of Boss Mining, Frontier, Comide, Swanmines, Congo Cobalt Corporation (CCC) and Metalkol RTR – (shareholding – 40% Republic of Kazhasthan, 50% private shareholders and 10% Congolese government) produces cobalt concentrates. According to ERG, in 2024, it paid a total of about USD 378 million to the Congolese government in terms of royalties and other charges.

Ruashi Mining (actionnariat 75% – Jinchuan Group International Resources Co., Ltd et Gécamines – 25%)

Chemaf (Chemicals of Africa, an Indian subsidiary of Shalina Metals where the Congolese government has a 5% stake) produces cobalt hydroxide. This company is in financial difficulty and is looking for a buyer.

Société des Terrils de Lubumbashi (STL)/GTL, whose majority shareholder has been Gécamines since 2019, produces cobalt in the form of alloys from slag.

Gécamines – a state-owned company that produces cobalt hydroxide. The latest statistics on its cobalt production date from 2022 with a production of 19,907 tons (EITI Report, 2022).

Entreprise Générale de Cobalt (ECG) – a state company, which buys the production from artisanal mining.

A Few Figures

The Ministry of Mines’ 2024 Annual Report indicates that the province of Lualaba exported 2,342,356.03 tons of copper, 200,972.04 tons of cobalt, and 1,109.94 tons of manganese, with a total value of USD 24,733,767,541.94 and generating, in terms of 100% royalties for the Congolese state, a sum of USD 1,059,505,878.76. According to the EITI (Extractive Industries Transparency Initiative), “budget revenues come from taxes based directly on turnover or profit, and are correlated with falls in the prices of cobalt, zinc, and copper.” Mining companies publish their payments to the government each year in order to comply with the EITI’s transparency principles.

Price in USD per ton of cobalt from 2018 to January 2026 according to London Metal Exchange (LME)

2018

2019

2020

2021

2022

2023

2024

2025

01/2026

98 000

35 000

28 000

52 000

70 299

36 160

24 000

52 300

56 292

Production of tons of cobalt from 2019 to 2024 (Sources EITI, Technical Coordination and Mining Planning Unit – CTCPM, Central Bank of Congo)

2019

77 964

2020

86 591

2021

93 145

2022

111 309

2023

139 838

2024

198 844

According to the DRC EITI and Standard & Poor’s (S&P), global revenues from the mining sector in USD billions from 2020 to 2024

2020

2 349 542 129 USD

2021

3 458 717 310 USD

2022

7 037 780 268 USD

2023

5 811 897 295 USD

2024

4 350 000 000 USD

The Deadly Sins of the Congolese Cobalt

Cobalt from the DRC has become one of the most controversial metals on the planet, to the point of being called the “blood diamond of batteries.” Essential for electric car and smartphone batteries, it nevertheless carries a sulphurous reputation. Its main fault? Having taken up residence in the Democratic Republic of Congo (DRC), a country considered unstable and poorly organized. However, cobalt is no more “toxic” or expensive than other strategic metals. It is mainly the conditions under which it is mined that bother some observers. They deliberately forget that 80% of cobalt production in Congo is industrial and only 20% comes from artisanal mining. And we often forget that the prices of this mineral—set in London—are completely beyond the control of the DRC. Market volatility, geopolitical tensions, and global industrial dependence are all factors that make it a symbol of the contradictions of the “green world.”

The specter of child labor

In the DRC, cobalt mining remains tainted by the sensitive issue of child labor. In 2016, Amnesty International, citing UNICEF figures from 2014, reported that 40,000 children were working in the mines of Kolwezi. This shocking figure has unfortunately been widely reported by several sources and media outlets since then. However, various investigations, including one by the German agency GIZ, have revealed that this number was greatly overestimated. More recently, a study by the International Labor Organization (ILO) counted approximately 6,200 children working in the mines of Lualaba and Haut-Katanga in 2024.

It should also be noted that 80% of Congolese cobalt production comes from industrial mines that operate in accordance with international standards. It is in artisanal mining that the entire production ecosystem remains a cause for concern. This sector alone accounts for 20% of cobalt production and suffers from structural problems: with little supervision and no formal mining areas, miners find it difficult to coexist with industrial mining groups, a problem that the government is struggling to resolve.

The weight of China

Another “sin” of Congolese cobalt is its dependence on China. Beijing is its main investor, refiner, and customer. According to the Central Bank of Congo, 57.3% of all Congolese exports were destined for China in 2023, and this trend shows no sign of slowing down. This dominance fuels fears among Westerners, who cite economic domination and strategic weakening of the country by other trading partners.

Meanwhile, Western automakers are touting the promise of “ethical” supply chains. This is a legitimate demand, but often a selective one: it is mainly because cobalt comes from the DRC that this ethics issue has suddenly become crucial.

Removal and/or Reduction of Cobalt in Batteries

Due to economic, geopolitical and ethical considerations, the electric vehicle sector is shifting its focus away from cobalt. As the most expensive metal used in cathodes, with a highly volatile price, cobalt has a significant impact on value chains.

Tesla was a pioneer in the field of electromobility, initially using the NCM 1:1:1 formula (1/3 nickel, 1/3 manganese, and 1/3 cobalt) in the cathodes of its Model S and Model X vehicles. The company then switched to the 8:1:1 architecture, which is much richer in nickel. In September 2020, Elon Musk took another step forward by announcing the large-scale adoption of LFP (Lithium-Iron-Phosphate) chemistry for the “standard” Model 3 and Y, a less expensive, cobalt-free technology.

On 29 January 2029, Elon Musk, who is facing fierce competition in China from BYD and in Europe from Volkswagen and BMW, announced that he will no longer produce the S & X models despite improvements made in 2025, including increased range, reduced noise, and smoother suspension. These are Tesla’s oldest and most expensive vehicles that used cobalt, and Elon Musk explained that he now wants to “… devote most of his investment to artificial intelligence, particularly autonomous driving technology, humanoid robots, and, ultimately, the chips that underpin these long-promised ambitions.” (CNBC News)

Following the lead of the Californian manufacturer, Ford, Volkswagen, and other major players in the automotive industry, BYD, a Chinese manufacturer, is also adopting LFP, a more secure and cost-effective raw materials supply.

Concurrently, the recycling industry is undergoing a process of consolidation. In Finland, a team from Aalto University has demonstrated the viability of reusing lithium electrodes containing cobalt. They have also developed a method for extracting this cobalt during recycling, thereby preventing its loss. In addition, manufacturers are investing heavily in R&D to move away from primary cobalt: Apple has committed to using only recycled cobalt in its future batteries.

It is evident that the global demand for cobalt will continue, though not necessarily the type mined in the Democratic Republic of Congo.

Congolese Government Suspends Exports of Cobalt Concentrates

In June 2025, the Congolese government took the strategic decision to suspend exports of cobalt concentrates, with a view to playing a major role in setting prices and thereby increase public revenues, combat fraud, and encourage local refining. However, the implementation of this suspension was undertaken without the necessary legal framework or the requisite infrastructure to ensure its effective operation. As a result, it was evident that there were more fundamental systemic issues: insufficient regulations, inadequate production control and erratic policy-making.

In the absence of a clear path forward, the government took the decision to lift the suspension and introduce export quotas. This move was made with a view to controlling production and influencing price stabilisation on the international market. As stated in the Central Bank of Congo’s Economic Outlook Note of January 16, 2026, the price per ton increased to $55,580, representing a 6.67% rise, due to the restriction of cobalt exports. However, this measure is contested by some mining companies.

Another issue that should be considered is that in November 2018, the Democratic Republic of the Congo (DRC) declared cobalt to be a strategic mineral. This means that, as such, its export royalty increased from 3.5% to 10% in order to take advantage of its higher market value, where applicable. However, no enforcement measures accompanied this decision, making it difficult to implement for the benefit of the country. Furthermore, the volatility of cobalt prices does not offer significant added value to the country. In 2023, the government imposed a 10% royalty fee. This measure provoked a negative reaction in the industry, which is obliged to comply with a government that has not yet improved its governance in the sector. This underscores the DRC’s challenges in effectively managing its most valuable asset.

The exorcism of Congolese Cobalt

Given the challenges facing Congolese cobalt, some may conclude that the “demon” in Congolese cobalt is not spiritual; it is institutional, economic and moral and lies in a set of structural factors :

Poor governance and corruption: a significant part of mining revenues disappear before reaching the Public Treasury.

Unfair contracts: Foreign multinationals reap the majority of the benefits, often with little local impact.

Lack of local processing: cobalt is exported raw, with no local added value.

Precarious and unstructured artisanal exploitation: Thousands of miners work in dangerous, informal and unprotected conditions.

Poor transparency: wealth becomes an instrument of power rather than a lever for development.

Exorcism in different steps :

A. Governance and transparency

Create a cobalt sovereign wealth fund, to be managed with transparency. This fund could finance infrastructure, education and health, rather than disappearing into opaque circuits.

Effectively fight corruption through an independent judiciary and regular public audits.

B. Industrialization and local added value

Create special economic zones dedicated to the local processing of cobalt (refining, batteries, technological components).

Require the disclosure of derivatives and their value.

Improving the energy sector, so that manufacturers can start refining cobalt in the DRC.

Massively train a qualified technical workforce to support this industrialization.

C. Social and environmental justice

Régularize the artisanal sector by establishing viable artisanal exploitation zones (ZEA) and by formalizing the artisanal sector, this providing security and a better livelihood.

Invest in the reconversion of mining communities and develop alternative activities (sustainable agriculture for instance and services).

Protect the environment: mining areas must include a clear plan for ecological rehabilitation and restoration.

D. Congolese economic diplomacy

Impose a “technological fee” : each company exporting Congolese cobalt should donate a percentage devoted to R&D which must be overseen by universities.

Create an African “cobalt cartel”, inspired by OPEC, so that producing countries have better control over prices and operating conditions.

In conclusion, considering all these factors, it is essential to ask whether the Congolese people have, in any way, already benefited from the revenues generated by this essential mineral, regardless of its price. Mining companies implement social development projects in the communities where they operate, as part of their corporate social responsibility mission. However, what are the implications for the rest of the country? I can safely say that the inhabitants of Mongala, Kwango, and other provinces know cobalt only by name and do not consider it a valuable asset for their livelihoods, as its benefits do not reach them. Yet cobalt must be mined for the benefit of the entire nation. Everyone should rejoice!

Therefore, the real exorcism is moral awakening: when the people demand accountability, when the elites serve and refuse to serve themselves, the demon will take flight. Congolese cobalt is not possessed. It is the system built around it that is. So the solution lies in transparency, local transformation, social justice, and resource nationalism. It is important to note that cobalt is a non-renewable mineral resource. If the DRC does not rectify its shortcomings, cobalt, like a true evil spirit, will haunt it until it is depleted in about five decades!

References

Léonide Mupepele, Monti, L’industrie minérale congolaise – Chiffres et défis, Tome 1, L’Harmattan RDC, Paris, 2013, p. 168

Journal Officiel, Loi no. 007/2002 du 11 juillet 2002 portant Code minier, CEDI, Kinshasa, juillet 2002

Décret N° 18/042 du 24 novembre 2018 du Premier ministre, déclarant le cobalt, le germanium et la colombo-tantalite « coltan » comme substances minérales stratégiques en République Démocratique du Congo. C’est le décret

Crundwell, F. K. et al (2011). Production of cobalt from the copper–cobalt ores of the central African Copperbelt. Extractive metallurgy of nickel, cobalt and platinum group metals, 377-391.

Banque centrale du Congo, Rapport annuel de 2023, Kinshasa

Banque centrale du Congo, Condensé d’informations statistiques, Kinshasa, 31/12/2025

Secrétariat général, ministère des Mines, Rapport annuel d’activités – Exercice 2024, Kinshasa

For any remarks, observations, corrections and comments, please send us an email at mkabamba@gmail.com or a message on Whatsapp at +1 647 767 8621 or +243 83 292 5377.